Government support: making home ownership more achievable

Buying your first home can feel like a big step - especially when saving a deposit and covering upfront costs seems out of reach.

The good news is there are government supports designed to help first home buyers get into the market sooner, with less money upfront.

Here’s how key supports work, and how they can potentially be used together when buying a first home.

The Australian Government 5% Deposit Scheme: buying with a smaller deposit

One of the biggest hurdles for first home buyers is the deposit. Traditionally, lenders require a deposit of 20% of the purchase price, or if your deposit is less, you may be required to purchase Lenders Mortgage Insurance (LMI) on top of your loan.

The Australian Government 5% Deposit Scheme, previously referred to as the First Home Guarantee or the Home Guarantee Scheme, helps eligible home buyers purchase a home with as little as a 5% deposit for first home buyers, or single parents with a minimum of 2% deposit plus associated costs (eg stamp duty) without paying LMI.

How it works

Instead of providing a full 20% deposit, the government can potenrially guarantee up to 15% or 18%, for eligible single parents, of the property value to the lender. This means:

- First home buyers only need to save a 5% deposit

- Single parents only need to save a 2% deposit

- The lender treats your loan as though you’ve contributed 20%

- You avoid the cost of LMI.

Importantly, this is not a cash payment. The government doesn’t give you money - the guarantee simply reduces the amount of deposit the bank requires. Refer to attached link for the current Property Price Caps for this scheme.

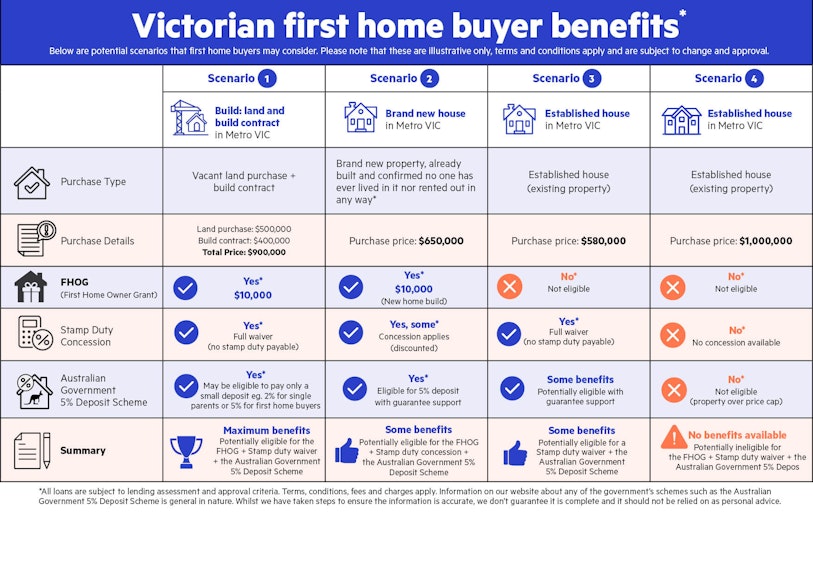

Example

Amelia and Carlos are looking to buy their first home and are considering their options from the table below:

Click here to view the full image of the table

*Please note that rules vary by state and can change at any time. The best place to confirm your exact eligibility is the relevant state revenue office website (refer to the bottom of page for state links).

The takeaway

The government schemes mentioned such as the Australian Government 5% Deposit Scheme, First Home Owners Grant (FHOG), and State Revenue Office’s (SRO) stamp duty concessions, which vary by state, can make a big difference to how soon you’re able to buy.

- The Australian Government 5% Deposit Scheme helps you buy with a smaller deposit

- Stamp duty savings or concessions can reduce upfront costs

- The FHOG gives extra funds (for example $10,000 in Victoria) if you’re buying a brand-new property or building a new property.

With the right guidance, these supports or schemes can move home ownership from “someday” to sooner than you might think.

Below is a list of state revenue office links for different states that might be helpful:

- First home buyer duty exemption or concession – SRO VIC

- First Home Buyers Assistance Scheme – Revenue NSW

- First home concession – QLD Revenue Office

- First Home Owner Rate – Revenue WA

- Home owner assistance – NT Government

- First Home Buyer - RevenueSA

At BankVic we’re happy to help you understand how the above ‘by State’ supports or schemes interact with federal schemes like the Australian Government 5% Deposit Scheme.

Ready to take the next step?

Reach out to our BankVic Home Loan Mentors to help you find out what type of home loan is right for you.

We’re here to help

If you have any questions about buying your first home, visit The Australian Government 5% Deposit Scheme or call 13 63 73 or Book appointment to make an appointment with a BankVic Home Loan Mentor.